+18 - Check if the casino you want to register with is eligible in your country.

Account restrictions happen for three distinct reasons: risk-based limits (operators think you’re beating them), T&C breach limits (you violated their terms), and fraud holds (something about your account triggered their AML system). Most players assume the first; the truth is usually more specific—and more defensible.

Operators apply risk scoring to your account in real time. That model watches five inputs: your win rate (anything consistently above 55% on EV+ bets raises flags), the odds you’re betting (if you’re consistently picking -110 or better and winning, that’s a synthetic signal), your account age (brand-new accounts with immediate 60%+ win rates get flagged faster), deposit patterns (sudden large deposits from crypto wallets flag differently than bank transfers), and withdrawal velocity (rapid deposits followed by massive cashouts trigger review). When your aggregate risk score exceeds their threshold—typically 65-75 points on a 0-100 scale—the operator’s compliance engine makes a decision: full restriction, limited odds only, bonus eligibility revoked, or enhanced KYC demand.

The operator isn’t accusing you of cheating. They’re protecting expected value. A player who consistently wins at +EV odds costs them money. Unlike a casino (where the house edge is fixed), a sportsbook’s margin depends on balanced liability. If you’re moving that balance against them, limits follow—not as punishment, but as risk management.

This matters because it reframes your appeal. You’re not fighting unfairness; you’re negotiating the operator’s risk tolerance. If your account was limited because of activity they explicitly allowed (matched betting, for example), that’s a T&C breach on their end—grievable. If it was limited because you won too much too fast on permitted betting, that’s within their rights (most T&Cs reserve this right), but escalable to dispute resolution if they didn’t disclose the risk model.

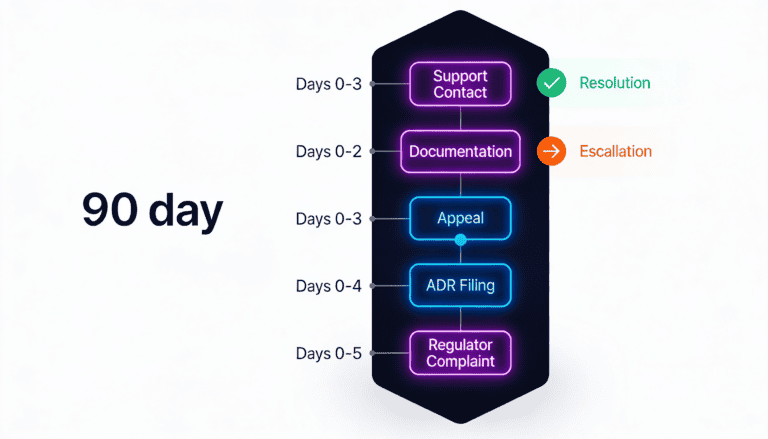

You have 90 days to move from operator contact to regulator complaint. The clock matters—most regulators require evidence that you’ve exhausted internal remedies first. Here’s the documented pathway.

Email the operator’s compliance address (usually compliance@[operator] or support@[operator]; check their terms page). Include your account number, a summary of your recent betting history (last 20 bets, win/loss ratio, average odds), and a direct request: “I received a restriction notice. Please provide the specific Terms of Service clause and risk factors that triggered this action.”

Most operators respond within 48 hours with a template response—”account restricted for breach of terms” or “unusual activity detected.” The vagueness is deliberate; they’re not obligated to reveal their risk model. Your job: match their response against their published T&Cs. Did they cite a clause you violated? Does that clause actually exist in your version of the T&Cs? Date matters—T&Cs change frequently, and operators sometimes apply old rules to new accounts.

If their reason doesn’t align with their published T&Cs, document it. Screenshot the T&C clause number, the date you read it, and the operator’s written reason. Create a side-by-side comparison. If they claim “matched betting violation” but their T&Cs don’t explicitly prohibit matched betting, that’s a weakness in their position.

Pull your account statement. Export your full betting history (most operators allow CSV download via account settings). Flag bets that allegedly triggered the restriction—were they within odds limits? Stake limits? Game restrictions? You’re building a case that either (a) you complied with all published rules, or (b) the rules were ambiguous and you acted reasonably.

Send a second email to compliance@[operator]. This one cites evidence. Structure it as: “Per your response on [date], my account was restricted for [cited clause]. However, my account history shows [specific evidence]. Additionally, your published T&Cs dated [date] do not explicitly prohibit [activity]. I request reconsideration based on this evidence.” Keep it under 300 words. Attach your documentation.

Some operators reverse restrictions at this stage if they realize they applied a rule they didn’t clearly state. Most don’t. If they don’t respond within 7 days, escalate.

Most licensed operators are contractually required to provide access to an independent ADR provider. Find yours by checking the operator’s terms page (usually listed under “Dispute Resolution” or “Complaints”). Common UK/EU providers: CIRSACOM, Olden Dispute Resolution, Interactive Disputes. Malta: Malta Gaming Authority’s dispute process. Curacao: Handled case-by-case; limited enforcement.

File your complaint with the ADR. You’ll pay a small fee (typically £25–100 for sportsbooks). The ADR reviews your case independently and makes a binding recommendation. Success rate: ~40–60% for account restrictions that hinge on T&C interpretation. The ADR won’t overturn operator decisions on risk management alone, but they will penalize T&C breaches by the operator.

If ADR doesn’t resolve it, escalate to the regulator. The pathway depends on the operator’s license:

Regulators care about three things: (1) Did the operator follow their own T&Cs? (2) Did they provide fair process? (3) Is this part of a pattern of abuse? If your case is one instance of vague T&Cs, success rate drops. If you can show the operator applies different standards to different players, or hides clauses in amendments, success rate climbs.

Bonus disputes fall into two buckets: ambiguous T&Cs that operators exploit and user misunderstanding of transparent T&Cs. The first is grievable; the second is on you. Here’s how to tell the difference.

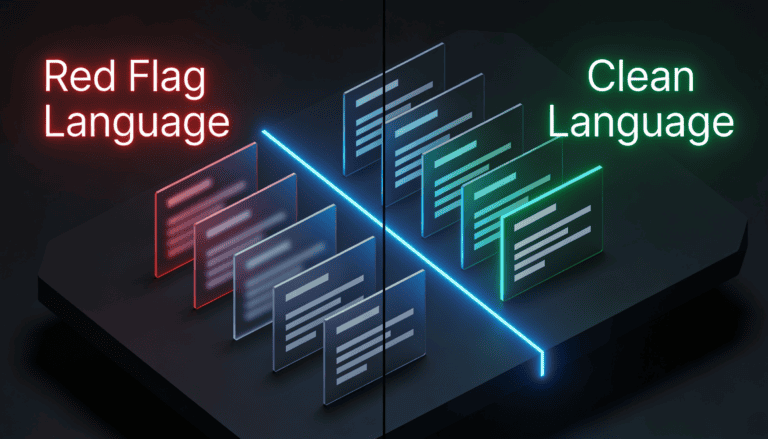

If a bonus T&C uses phrases like “reasonable wagering requirements,” “certain games may not contribute fully,” “operator reserves right to modify,” or “minimum odds may apply,” that’s ambiguity-by-design. The operator is preserving discretion. When you dispute a forfeited bonus later, they’ll cite the vagueness and claim it was “your responsibility to verify exact terms.”

Clean bonus language looks like: “Bonus requires 35x wagering. All slots count 100%. Live dealer games count 50%. Sports bets count 0%. Wagering window: 30 days. Bonus forfeited if unused by [exact date].” Specific numbers, explicit game weightings, hard deadline. Disputes on clean bonuses are usually resolvable because the T&C violation is objective.

You claimed a bonus, wagered to the requirement, and then your bonus balance disappeared. Why?

Contact support with a single, specific question: “Per your T&Cs dated [date], my bonus should have cleared because [state reason with evidence]. My account shows [exact bonus balance, date]. Please explain the discrepancy or restore the bonus.” Attach a screenshot of the T&C clause and your account statement showing the bonus transaction.

If they refuse, file ADR. Bonus disputes are among the most ADR-friendly complaints because they involve clear contractual language. Success rate: 65–75% if your evidence is solid.

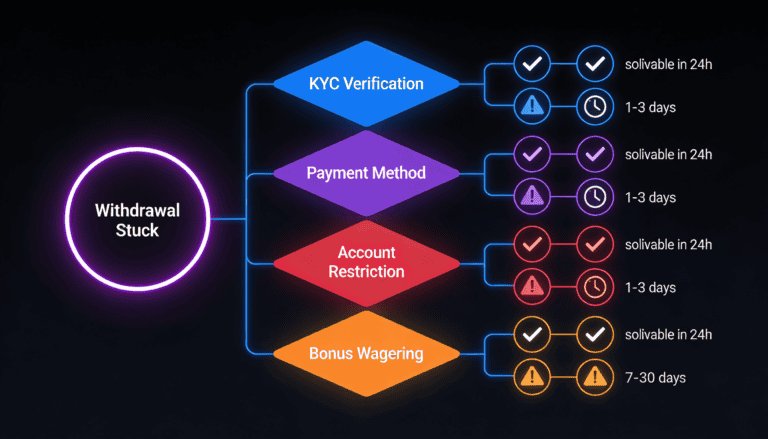

Your withdrawal request was submitted. It’s been 48 hours—or 5 days—and nothing. The status page says “pending.” Support says “it’s being reviewed.” Here’s how to decode what’s actually happening and which issues are solvable in 24 hours vs. which require escalation.

The most common reason. Operators must verify identity under AML/KYC regulations. If your withdrawal is stuck on KYC, you’ll see a message like “Account under verification” in the cashier. This happens when:

Solution: Go to Account > Verification or Compliance. Upload a clear, well-lit photo of your ID (passport or driver’s license; both sides if required). Upload a recent utility bill or bank statement showing your name and current address. Make sure the name and DOB match exactly. Most operators process within 2–4 hours; some take 24. Do this immediately. If rejected a second time, contact support with the exact error message (e.g., “Document quality too low”) and ask for specific guidance on what they need. Some operators will tell you to try again; some will escalate to manual review.

Your chosen withdrawal method declined. Why? Bank transfers sometimes fail if your account name doesn’t match exactly. E-wallet withdrawals fail if the e-wallet account has limits or is flagged for suspicious activity (not on the operator’s end—on your e-wallet’s end). Credit card chargebacks have additional holds. Crypto payouts rarely fail but can be slow if the blockchain is congested.

Solution: Try an alternative method. If you deposited via Visa, try withdrawing to a different e-wallet (PayPal, Skrill, Wise). If the first withdrawal fails for any reason, contact support immediately and ask to try a different method. Most operators allow 2–3 active withdrawal methods. Switch and retry. Crypto withdrawals are instant (usually under 2 minutes) but require you to trust the blockchain—if you’re unfamiliar, start with a small test withdrawal first.

Your withdrawal stuck and you can’t access the account. This is a restriction block. Withdrawals are disabled as part of the account action. You’ll see “withdrawal unavailable” or won’t find the cashier option at all. This requires the escalation pathway described in the Account Restrictions section above—contact compliance, request written reason, appeal, file ADR if needed. Timeline: 3–7 days at minimum; up to 90 days if you escalate to regulator.

Check your account status. If a bonus is active and not yet wagered to requirement, most operators block withdrawals until the bonus is cleared. Why? Because they need to know: are you wagering the bonus? If you abandon it unclaimed, the operator’s liability drops. If you claim it but don’t wager, they’re owed the wager activity. Solution: Check your bonus T&Cs for the exact wager requirement (usually 35x–50x). Go to the cashier and confirm whether a bonus is active. If yes, you have two options: (a) complete the wager (may take 2–4 hours depending on your betting speed), or (b) forfeit the bonus (some operators allow this via a checkbox; others don’t). Forfeiting is instant; withdrawal then processes. Most players do this if the bonus requirement is unreasonable relative to their bankroll.

Rarely, a withdrawal gets stuck with no explanation and support is evasive. This usually means the operator’s AML system flagged your account as high-risk. Possible triggers: deposits from multiple payment methods in short succession, withdrawal to a different person’s account, unusual deposit amounts ($5,000 suddenly after months of $50 deposits), or an automated match against sanctions lists.

Solution: Ask support directly: “My withdrawal is pending. Has my account been flagged for AML review? If yes, what documentation do you need from me?” If they confirm an AML hold, they’ll usually ask for: proof of income (payslip, tax return), bank statements, and source-of-funds documentation. Provide these. Processing takes 7–14 days. If they refuse to explain or provide a pathway, escalate to ADR and regulator (see escalation pathway above). AML holds are legitimate, but operators must justify them and provide a process for clearance.

You’re researching an operator before you deposit. Or you’ve had a bad experience and want to know if it’s a pattern. Here’s where peer data lives and what each source actually tells you—and what it doesn’t.

UKGC Operator Search (ukgc.org.uk): Type the operator name. You’ll see license status (active, suspended, revoked), license number, and a complaints register. This is the ground truth for UK operations. If an operator’s license is revoked, they’re actively breaking UK law. If they’re suspended, they’re in remediation. Active license means they’re currently compliant with that regulator’s standard. Note: License status doesn’t tell you about disputed withdrawals—that’s in the complaints log, which is anonymized. A high complaint count doesn’t mean the operator is bad; it might mean they operate at scale and attract more complaints statistically.

Malta Gaming Authority (mga.org.mt): MGA licenses cover EU operations and many offshore markets. Same principle: verify license status, read the conditions. MGA enforcement is stricter than Curacao but more limited than UKGC. A Maltese license is a meaningful compliance signal.

Curacao eGaming Authority: Weakest enforcement tier. A Curacao license exists; enforcement doesn’t. If an operator is Curacao-only, treat them as higher-risk. This doesn’t mean they’re fraudulent—many are legitimate—but your recourse is limited if things go wrong.

Reddit r/sportsbook: Search the operator name. Read the last 20 threads. You’re looking for patterns, not single complaints. One user complaining about gubbing (account limitation) is noise. Ten users reporting identical bugs with withdrawals in the last 6 months is signal. Pay attention to timestamps; old complaints may be irrelevant if the operator fixed the issue.

Trustpilot (verified reviews, 200+ votes): Filter for reviews with 200+ votes (this filters out fake reviews and noise). Read the last 30 verified reviews. Average rating under 3.0 and >50% complaints about withdrawals or limits? That’s a red flag. Average rating 4.0+? Likely operational. Note: Trustpilot’s review base skews toward people with strong opinions (very satisfied or very angry), so pure averages can mislead. Read 5–10 specific verified reviews to triangulate.

AskGamblers: Player-submitted operator database. Each operator has a safety rating. This is community consensus, not regulatory data. AskGamblers is useful for aggregating patterns (“100+ players report account limits within 30 days of sign-up”), but don’t treat it as gospel. Cross-reference with UKGC/MGA data.

Platform-specific forums, Discord servers, Twitter sentiment. These are anecdotal. Use them only to triangulate findings from Tier 1 & 2. If Tier 1 shows a license is active, Tier 2 shows mostly positive reviews, but a Discord has three people complaining about slow payouts, the Discord data is valuable context—it’s a specific issue to watch for—but it doesn’t override the stronger signals from regulatory and verified community sources.

You’ve exhausted operator support and ADR. Now you’re filing with UKGC or MGA. Here’s what regulators need to see; without it, your complaint stalls.

UKGC (ukgc.org.uk/contact-us): Use the online complaint form. Attach your documentation bundle as a single PDF. Write a 500-word summary of your issue: “I signed up for [operator] on [date]. I claimed a bonus on [date]. The bonus was forfeited on [date] for the following reason [operator’s claim]. However, the published T&Cs state [exact T&C language]. Based on this, I believe the operator breached their contract. I’ve provided evidence below.” UKGC responds within 8 weeks; you’ll get a case number.

MGA (mga.org.mt): Similar process, but slower. MGA’s complaint pathway is less streamlined than UKGC’s. Timeline: 12 weeks+.

Success rate for well-documented complaints: 40–60% for account restrictions that involve T&C disputes; 70–85% for withdrawal delays that involve KYC mistakes or payment method errors.

If these issues are causing frustration or financial stress, pause. Most licensed operators provide tools: deposit limits (set a daily/weekly max), session limits (auto-logout after 1 hour), loss limits (warn when you’ve lost £X), and self-exclusion (temporary or permanent account suspension).

These work. They’re enforced by the operator and cross-operator databases (like GAMSTOP in the UK) block you across multiple sites. If you’re experiencing repeated account disputes, losses, or are chasing losses through escalation processes, that’s a signal to use these tools.

Resources: GAMCARE (gamcare.org.uk), Gordon Moody Association, National Council on Problem Gambling (NCPG, 1-800-522-4700 US).

Operators apply risk limits to protect expected value. A sportsbook’s margin depends on balanced liability across bets. A player consistently winning at +EV odds costs them money, especially if the win rate exceeds 55–60% over 50+ bets. When this pattern emerges, the operator’s risk model flags the account and applies limits: reduced odds, bonus ineligibility, or full restriction. This isn’t fraud detection; it’s portfolio management. Most operator T&Cs explicitly reserve this right (“We may limit or restrict accounts at our discretion”). The limitation is within their rights if disclosed, but the risk model itself is usually not disclosed. If you were limited and believe the reason wasn’t disclosed in T&Cs you read at sign-up, you have escalation grounds.

Timelines vary by method: Bank transfers typically process within 3–5 business days (some same-day). E-wallet transfers (PayPal, Skrill): 1–24 hours. Crypto: Usually instant (under 2 mins); sometimes slower if blockchain congested. Card withdrawals: 5–7 business days. If you haven’t received payment after the operator’s stated timeline + 2 business days, contact support. If support is unresponsive after 48 hours, escalate. Never wait more than 10 days before filing a formal dispute. Most regulator complaints require evidence that you contacted the operator at least once.

Limit: Operator restricts your account but keeps it open. You can’t bet or withdraw; your funds remain in your account. Timeline to reverse: unclear (could be days, weeks, or permanent). Closure: Operator terminates the account. If there’s a balance, they must process a final withdrawal (usually within 30 days per regulation). If balance is zero, they can close it immediately. Limits are negotiable (escalate to regulator, sometimes reversed). Closures are harder to reverse but possible if the closure process was unfair. Always escalate a closure quickly because regulators prioritize accounts with trapped funds.

Yes, if you can prove it. Regulator complaints and ADR decisions often award refunds if the operator violated their own published T&Cs and you acted reasonably in reliance on them. Example: T&Cs state “minimum odds -110” but operator restricts you after you consistently bet at -115. You have grounds for recovery. Success rate: 65–75% if documentation is strong. However, if the operator’s breach is small (e.g., they owe you £50 of a £200 bonus), some players drop the case because escalation is time-intensive. Track your damages before escalating: “I claim £X in forfeited bonus, £Y in restricted winnings, £Z in time costs.” Regulators are more likely to act if the amount is material (£100+).

Verify license status first (UKGC, MGA). This is ground truth. Then cross-reference with Trustpilot (200+ verified votes) and Reddit r/sportsbook for patterns. AskGamblers is useful for aggregating player feedback but treat it as secondary. Twitter/Discord is anecdotal—useful for specific issues (e.g., “withdrawal bugs reported by three users”) but not for overall operator assessment. Never base a decision on a single source. Use this hierarchy: Regulatory data (primary) → Verified community data (secondary) → Informal forums (tertiary, context only). If Tier 1 and Tier 2 align, you have confidence. If they conflict, assume the conflicting data is recent (community feedback changes as operators improve or deteriorate) and research current status.

Essential: (1) Account statement (full transaction history), (2) Screenshots of T&Cs dated with URL, (3) All operator correspondence (emails from support/compliance with timestamps), (4) ADR recommendation if filed, (5) One-page side-by-side comparison of your claim vs. operator’s response vs. T&C language, (6) Timeline showing when you reported the issue and how the operator responded. Regulators process complaints with weak documentation slowly or dismiss them. With strong documentation, they prioritize your case. Spend 2–3 hours assembling this bundle before filing; it halves your resolution timeline.

Read for specificity. Fair bonus T&C: “Bonus requires 35x wagering. All slots count 100%; live games 50%; sports bets 0%. 30-day deadline. Bonus forfeited if unclaimed.” Unfair bonus T&C: “Reasonable wagering requirements. Certain games may not contribute. Operator reserves right to modify. Minimum odds may apply.” Unfair language gives the operator discretion. Specific language (numbers, percentages, deadlines) removes discretion. If the T&C uses vague language, calculate the wager requirement yourself: if the operator claims “35x” but doesn’t specify game weightings, assume 50% contribution on average and calculate worst case. If the calculation exceeds your expected play, pass on the bonus or claim it with reduced expectations. In disputes, specific T&Cs almost always win; vague ones are losses waiting to happen.

ADR success rates by issue type: Account restriction due to T&C breach, 55–65%. Bonus disputes (forfeiture, wagering), 70–80%. Withdrawal delays (KYC/payment), 85–90%. Account closure appeals, 40–50%. Regulator complaints (UKGC/MGA) have similar rates but take 8–16 weeks vs. ADR’s 4–6 weeks. ADR is faster; regulator complaints have more enforcement power (they can revoke licenses). For time-sensitive disputes (withdrawal stuck, funds inaccessible), ADR first. For systemic issues or repeated patterns, regulator complaint second. For small-value disputes (

Yes. Matched betting (betting the same event at different sportsbooks to guarantee profit via bonus exploitation) is not explicitly prohibited in most T&Cs, but operators flag the betting pattern: multiple bets on identical outcomes across different odds, near-zero variance, rapid bet placement. The operator’s risk model sees this as suspicious and applies limits. Most operators have moved toward explicit prohibitions of bonus abuse (including matched betting) in updated T&Cs. Check before matched betting: does the operator’s current T&C prohibit “bonus abuse,” “betting the same event across multiple accounts,” or “arbitrage betting”? If yes, matched betting is risky. If no explicit language, you’re exploiting gray area; limits are possible but escalable if the T&C didn’t warn. New UK operators increasingly prohibit it explicitly. Established operators may not have updated T&Cs.

Account restrictions, bonus disputes, and withdrawal delays follow predictable patterns. Most are resolvable if you document your case and escalate correctly. Regulators exist to enforce T&Cs; use them.

If your account is restricted: Email support for written reason. Document how their reason aligns (or doesn’t) with published T&Cs. If misaligned, appeal. If they refuse, escalate to ADR within 30 days, then regulator. Timeline: 3–90 days depending on escalation.

If your withdrawal is stuck: Diagnose the cause (KYC, payment method, restriction, bonus, AML). KYC issues are solvable in 24 hours with documentation. Restrictions require the escalation pathway above. Don’t wait more than 10 days.

If a bonus was forfeited unfairly: Check whether your T&C version was specific (numbers, percentages) or vague (discretionary). If specific and you complied, escalate to ADR. Success rate: 70–80%.

Before you join an operator: Verify UKGC or MGA license. Cross-reference Trustpilot (200+ verified reviews) and Reddit r/sportsbook for patterns. Read T&Cs for clarity (specific language = lower dispute risk). Check the published ADR provider. If any of these is missing, you’re increasing your risk.

If these disputes are recurring or causing stress: Set deposit limits or use GAMSTOP to block yourself across multiple operators. Dispute escalation is time-intensive and mentally taxing. The goal is to bet sustainably, not to fight operators constantly.

Gambling Awareness: Problem gambling can cause significant financial and personal harm. If you’re experiencing difficulties with control, chasing losses, or betting beyond your means, reach out: GAMCARE (gamcare.org.uk), NCPG (1-800-522-4700 US), or Gordon Moody Association. Most licensed operators provide deposit limits, session limits, and self-exclusion tools. Use them.

Secod has streamed and tested games on Stake extensively, giving him direct insight into the platform’s bonuses, features and gameplay conditions. His experience ensures every Stake review reflects real usage rather than surface level analysis.

© 2018-2026 bonustiime.com

![]()

Casiibro is currently offline.

Learn more about them on their channel!

▶ Visit Casiibro's channelOr head to the Stream Hub.